Your Guide to The Miller Act Vs. The Little Miller Act

If you are somehow related to construction and you have a specialization in dealing with government contracts then you must have probably heard about the miller act. We will discuss the miller act vs. the Little Miller Act, both versions which can make an impact on your work.

Also, read for The Building Blocks of Modular Construction: Contractual & Lien Considerations

What is the Miller Act?

The miller act is a protector of construction parties from the first and second-tier who are looking to recover the outstanding debts. In the miller act, the commanding contractor will have to obtain the two surety bonds; one of them is a payment bond and the other is the performance bond. Under the performance bond, the satisfactory completion of the project is agreed on a duly sign contract. Now under the payment bond, all the suppliers and sub contractors are assured of their due payment. This miller act was passed in the year 1935. States over the years though started to bring upon the changes. All those state-wise changes were known as the little miller acts.

The Miller Act vs. the Little Miller Act

Under the miller act, contractors are expected to secure payment bonds for contracts that are more than $100,000. For other protection of payments, a contract between $30k to $100k is provided. If the payment is not made to suppliers or sub contractors, they can straightaway sue the contractor in district US court.

Under the little miller act, there are different statutes under different states. They all have their own set of rules and guidelines. So it comes down to the fact that if the construction project is being implemented under the federal government, the miller guidelines are followed and if the project is state-sponsored, the little miller act is put in place.

Little Miller Act Differences among States

It is very clear that the little miller act will vary from state to state and one is advised to study the specific guidelines laid by the state under the act before the project is commenced. Also, one should make sure that the entire legal obligations under the act are rightfully met. Things to look upon are-

- Contract amount requirement

The amount of payment bond that has to be secured by the contractor under the federal miller act can be different in each state. For example, that bond payment in Missouri can be around $25000 and in states like Tennessee, the amount could exceed almost $100,000.

- Bond claim filing/notice requirements

The deadline to file a bond claim is another variation that differs with each state. Let us consider an example of it. in Illinois, one is expected to file bond claims within the period of 180 days when the last work or furnishing is completed. But in contrast, the claimant in Florida will not have to file any notice in this regard. In Louisiana, the deadline for filing is of 45 days.

- Bond claim statute of limitation

This means the deadline to file the lawsuit for the bond claim. Each state has its time frame within which one is expected to file the bond claim. The little miller act will have all the details concerning each state.

How to File Little Miller Act Bond Claims

One should have a clear understanding of the eligibility to file the bond claim. Few states allow only the construction parties of a first and second tier to file the claim. Hiring an attorney will be much more advisable as he will have all the experience to share in construction disputes.

We at the National Lien and Bond Claim System will be happy to help you in such cases. We also have a great team to deal with cases related to a lien in Texas and Florida. We would be glad to help you in every way.

Also, read for

- Questions about the Impact of Sloan v. Liberty Mutual

- What Are Liens and How Can They Impact Your Property?

Related Articles

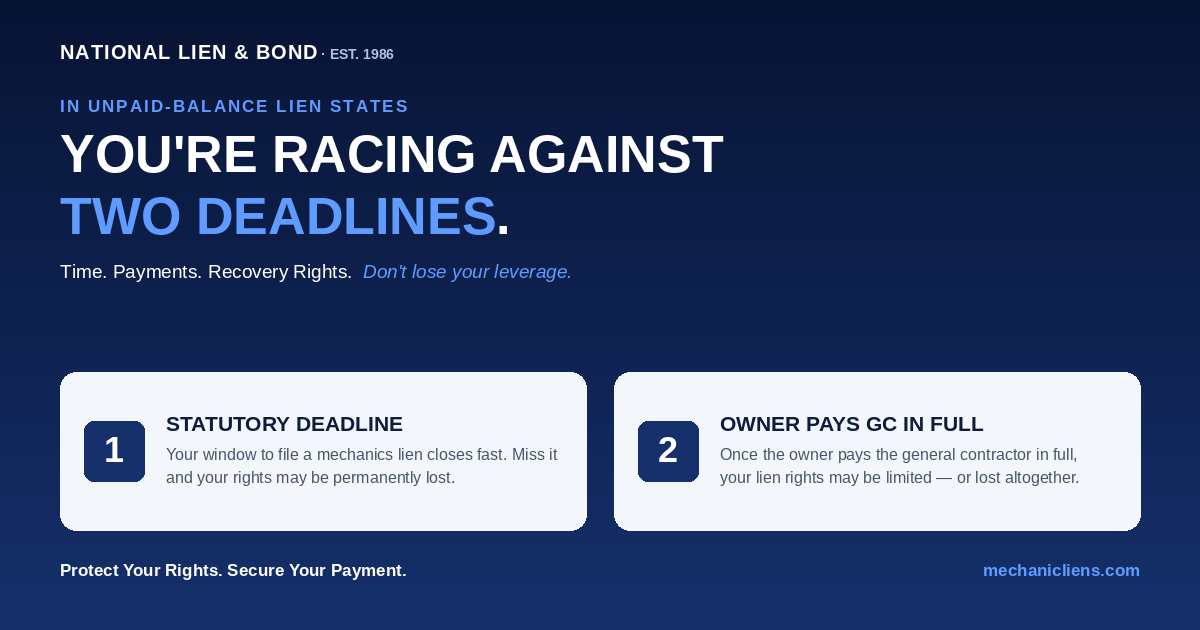

Unpaid-Balance Lien States: Why You're Racing Against Two Deadlines, Not One

In an unpaid-balance lien state, the calendar deadline to record your lien is only half the race. The hidden second deadline is the moment the owner finishes paying the general contractor - because that payment can shrink or erase the fund your lien attaches to. This guide explains both deadlines, why subcontractors and suppliers lose money even when they file 'on time,' and the notice-and-timing strategy that protects your leverage.

Read Article

Connecticut Mechanics Lien Law: Notices, Deadlines, Lien Rights, and Contractor Registration

Connecticut treats original contractors and lower-tier claimants differently. This guide covers the lower-tier notice of intent, the 90-day certificate recording deadline, the 30-day owner-service requirement, the one-year foreclosure-and-lis-pendens deadline, the lienable-fund limit on subcontractor liens, who can claim, and how Home Improvement Act and New Home Construction registration affect enforcement.

Read Article

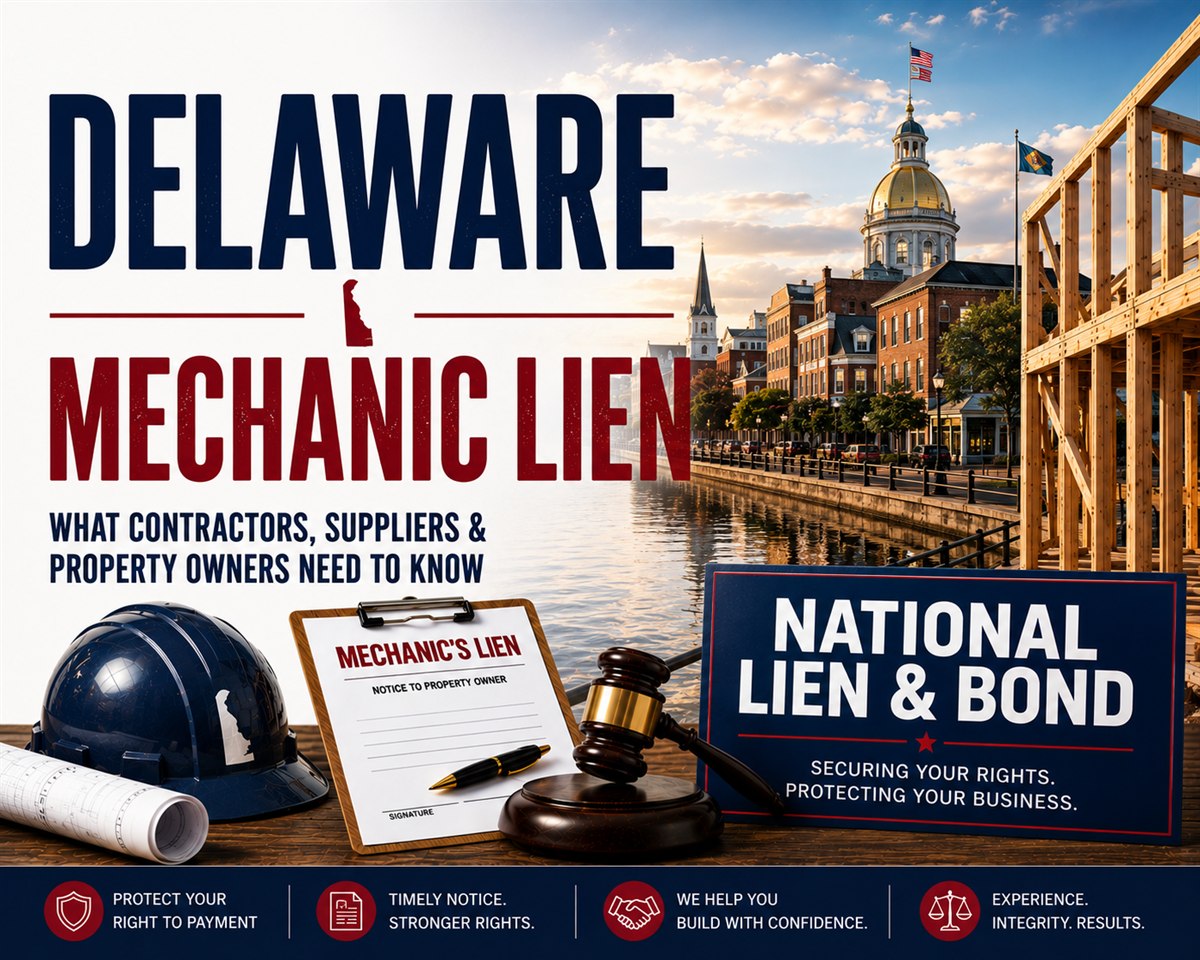

Delaware Mechanics Lien Law: Statement of Claim, Deadlines, Lien Rights, and Contractor Registration

Delaware enforces mechanics liens through a strictly construed statement of claim filed in Superior Court. This guide covers the 180-day and 120-day filing deadlines, the prior-written-consent rule for tenant work, the statement-of-claim pleading elements, the $25 threshold, who can claim, and Delaware contractor registration and business licensing.

Read Article